Co-ops: High on housing, low on profit

Cooperative housing minimizes the role of profit in housing while foregrounding actual maintenance costs.

The housing crisis is not just about supply, but control.

A major rift in housing discourse continues to be whether new supply is a silver bullet or the opposite—a mechanism that increases housing costs. We won’t attempt to answer this question today, but we will talk about a great alternative to the current approach of ‘build baby build’.

The solution to the persistent crisis of housing is not merely quantitative. Instead, the qualitative details are just as crucial: what kind of units are built, who owns them, and who finances them? On both the political left and the right, there is recognition that paying ever-increasing rents to global investment firms who continue to outbid regular folks for homes isn’t a great model. Yet, there hasn’t been adequate attention to a longstanding housing model that offers a way out of the housing trap: cooperatives (co-ops).

Cooperative housing minimizes the role of profit in housing while foregrounding actual maintenance costs.

Residents of co-ops do not own their physical units as direct property, but are instead members of an association that owns the entire housing structure. As part of a non-profit cooperative, members (1) own a share of the corporation, and (2) have exclusive rights to their housing unit during their membership. In most cases, all co-op residents are voting members of the cooperative’s non-profit organization. This allows for the housing model to be run democratically, with voting power usually allocated as ‘one person, one vote.’ If the co-op board proposes to raise the monthly housing fee to start saving for a new roof or HVAC system, all residents would get to vote on this proposal.

The Playbook for Cooperative Development (2022) offers a wealth of information about the housing model

- Residents own 100 percent of the cooperative, while the cooperative owns 100 percent of the property title.

- Homeowners pay monthly charges consisting of their proportionate share of one month’s worth of the cooperative’s annual budget.

- Monthly payments are referred to by different co-ops as occupancy charges, carrying charges, housing charges, assessments, or maintenance charges.

Co-ops let residents control their own housing, not landlords

There are different co-op models, primarily (1) market rate and (2) limited equity. Market rate co-ops have no restriction on the unit’s appreciation or re-sale value, allowing shares (analogous to the housing unit) to be sold at market value. Limited equity co-ops apply at least some restriction to the re-sale value to preserve affordability.

Consider first the model for the typical existing apartment building. A landlord receives revenue from the wages of tenants in exchange for offering a place to live. In Ohio, the rent can go up as much as the landlord likes, as often as the landlord likes. Landlords don’t need to justify the rent hike, demonstrate investment in the unit/building, or provide evidence that the cost of doing business has actually increased in relation to any rent hike. The lucrative earning period comes when the mortgage is paid off. Even after the property is entirely paid for, the rent continues to climb in perpetuity.

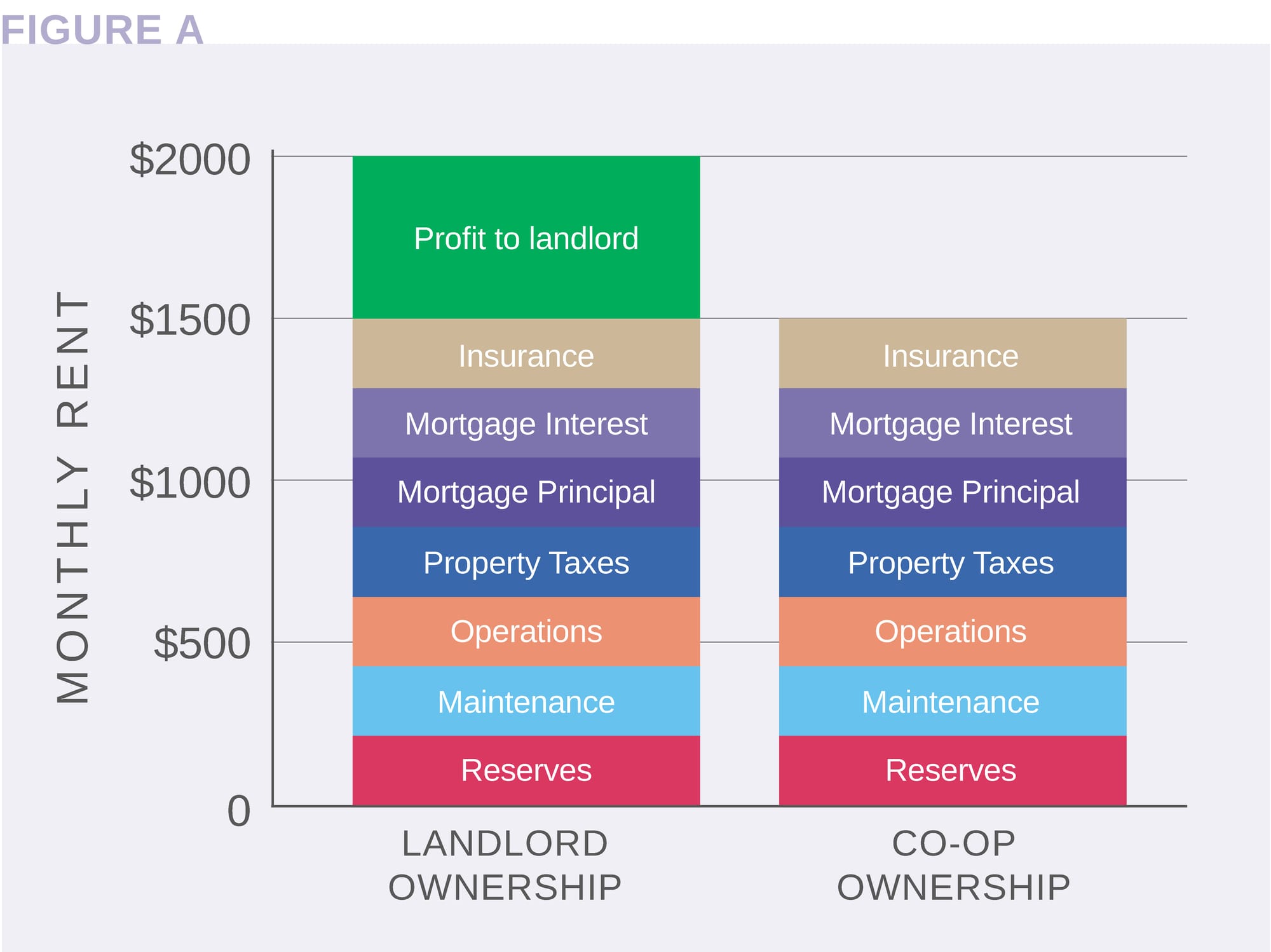

Typical equation of landlord-owned housing

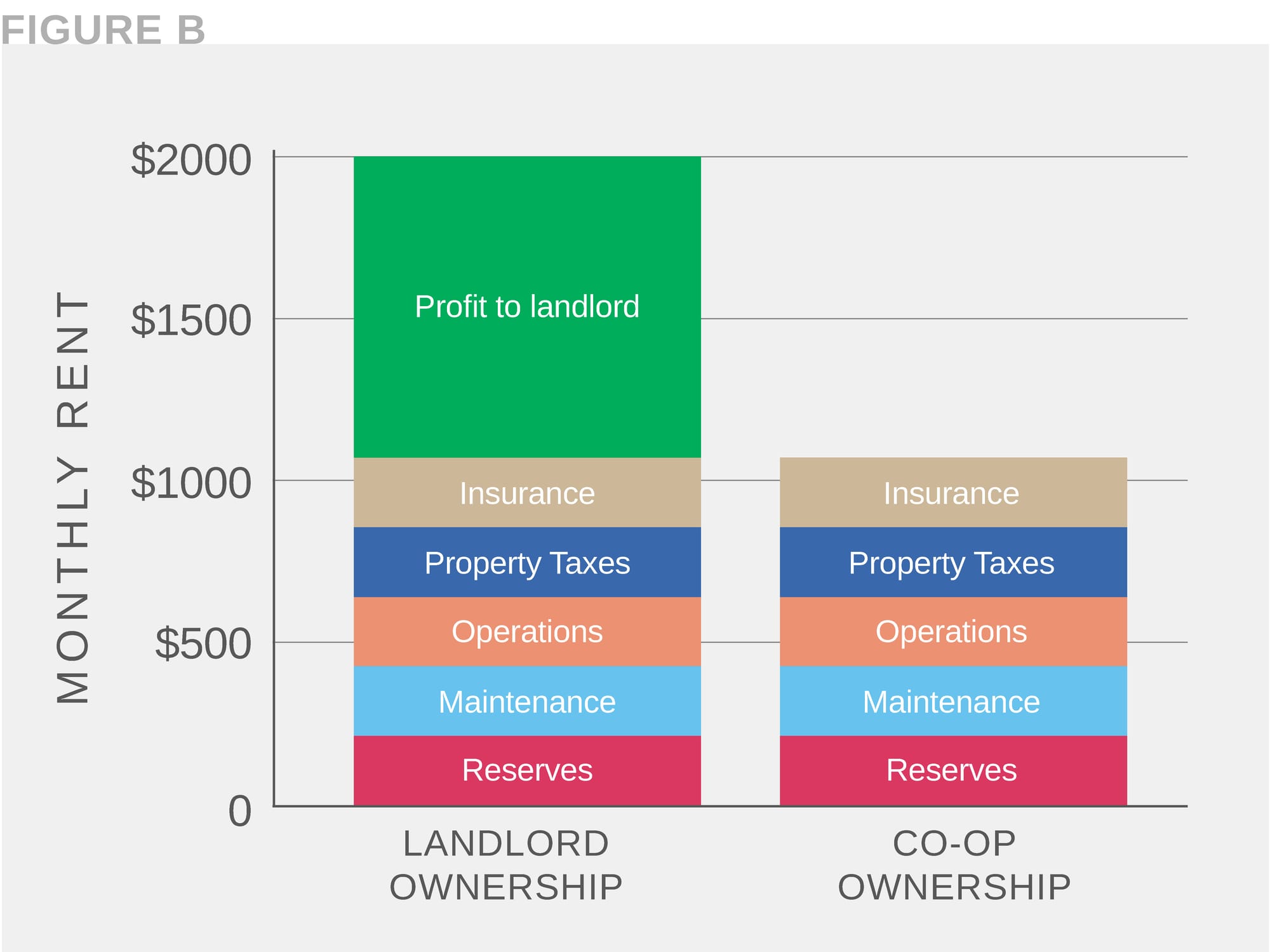

The illustration below is a general representation of the many costs that go into housing ownership as a portion of a tenant's monthly rent. Figure A demonstrates the savings possible in the co-op model by removing the slice of profit that goes to the landlord. Indeed, "because cooperatives operate at cost, cooperative carrying charges are often 15 to 25 percent or more below rental market rates" (MAHC). Figure B demonstrates the same allocation of tenant monthly rent after a property's mortgage is paid off. Under landlord ownership, the amount of profit going to the landlord increases substantially. But under co-op ownership, the cost of housing is able to stabilize or decline once a mortgage is paid off since the monthly charge is not tied to a fictitious "market rate" or determined by an algorithm.

Figure A: General representation of actual housing costs as a portion of monthly rent on a property with an active mortgage. Figure B: Same, but on a property without an active mortgage (owned outright). Costs are not intended to be proportional to one another, merely a representative listing.

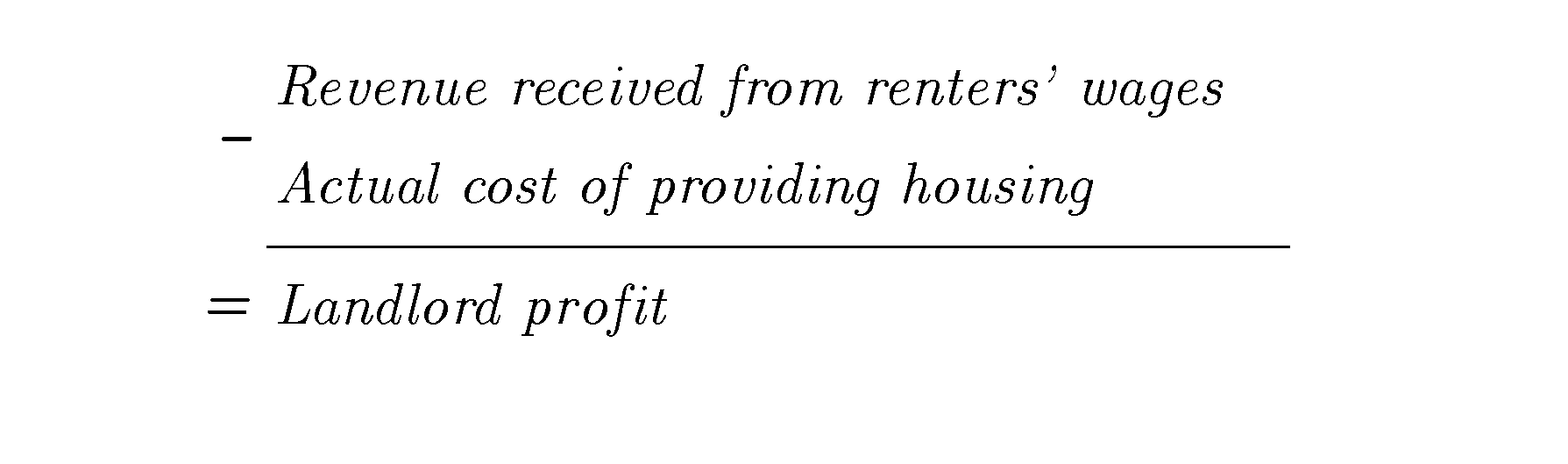

The owners of rental housing exhibit strong class solidarity by colluding in price-setting through their use of software like RealPage. The price a tenant pays for their monthly rent is not reflective of the actual costs of providing housing: property taxes, utilities, ongoing maintenance, saving for future expenses, unit turnover, amenities, etc. Instead, the price is set by “the market,” which today is often determined by an algorithm that many landlords agree to accept when they use RealPage. This strategy allows the price paid for housing to dramatically exceed the actual cost of providing housing. The difference between these two things equals landlord profit.

Now let’s turn to the cooperative housing model.

In most co-op cases, a nonprofit organization is created to build, own, and operate a multifamily housing structure. Imagine that you find a group of 50 households who want to start a co-op. You all agree to form a nonprofit entity, create a board, and contribute money to the organization that would then use that money as a downpayment on a construction loan from a bank to construct a 50-unit building.

After the building is built, you’d all move in and be members of the cooperative association. As a member, you would own shares in the corporation and have exclusive use of your home. The monthly fee you pay is not rent, but it goes to the nonprofit association that you’re a member of. This fee helps ensure the financial security of the association and the building itself, especially for major repairs that may be needed down the road.

The major difference between a rental and a co-op is that a co-op removes the landlord. After all, landlords aren’t producing anything. They’re using their access to capital (often merely debt) to own something, then charge others ever-increasing prices for the use of an essential human need (i.e. lording over the land). The co-op model reclaims housing by taking out the pesky middle-man skimming off the top.

Why is being a cooperative member better than renting? (click to expand)

- Lower monthly costs: Because cooperatives operate at cost, cooperative carrying charges are often 15 to 25 percent or more below rental market rates.

- Tax deductions: For income tax purposes, cooperative members are considered homeowners. As such, they can deduct their share of real estate taxes and mortgage interest paid by the cooperative, in addition to any interest paid on a share loan.

- Home equity: In a market equity or limited equity cooperative, members can accumulate equity in their dwelling unit.

- Security: Tenure is secure, within the guidelines of the law, cooperative bylaws, and occupancy agreements.

(Excerpted from the Midwest Association of Housing Cooperatives)

Have there been co-ops in Columbus?

After a thorough search through the archives, we were not able to find evidence for cooperative housing in Columbus’ past (please correct us if we’re wrong!). There were, however, some projects informally called “cooperatives” built under Section 236 of the National Housing Act that had income requirements for renters. Despite being called cooperatives, these functioned more like typical rentals. It seems that Columbus developers only took advantage of the rental housing option, not cooperative housing owned by nonprofit member associations. By 1999, many of their owners chose to stop participating in the income-restriction program (Thomas, Dispatch, 22 August 1999).

Located near the intersection of Morse and Sunbury Roads, Winchester Station was originally financed using the Section 236 program. Today, residents are members but the membership fee functions more like a security deposit (Personal correspondence, 1 July 2025).

In 1950, Congress was considering a proposal to fund a co-op financing program that would have made $2 billion available for lending to housing cooperatives.

A radio-television forum in Columbus invited two men supportive of the proposal and one opposed to discuss this proposal (Dispatch, 6 Feb. 1950, p. 12). The proponents explained that offering lower interest rates for cooperatives to borrow money would benefit Americans by reducing the cost of housing and constructing countless units outside of the control of landlords. The opponent, a local realtor, claimed that such a proposal would "put private investors at a disadvantage."

Note, his criticism was not about the effect on Americans who need housing. It was only about the reduced potential for profit by the real estate sector. Unsurprising, the real estate industry is generally opposed to putting housing back in the hands of residents. Co-ops provide housing while reducing the opportunity for profit by removing the housing middlemen—the owners, the managers, and landlords who create nothing.

Cooperative housing coming to Columbus

Despite housing co-ops not really being part of Columbus’ past, there are efforts to ensure that co-ops have a place in Columbus’ future. Motherful Village is a pilot housing cooperative funded by the RISE Together Innovation Institute that is currently in the planning stages.

Learn more about housing cooperatives

- Working Class Utopias (Fogelson, 2022)

- Home Base: The Playbook for Cooperative Development (2022)

- Cooperative Housing International

- National Association of Housing Cooperatives

- Research on cooperatives from OSU Extension (includes interactive map)

- Cleveland Owns

- Multifamily homeownership research (California Community Builders)

- Midwest Association of Housing Cooperatives

Notable News 🗞️

Local + Regional

When Wall Street is your landlord: How institutional investors impact central Ohio

29 June 2025, The Columbus Dispatch

- Work set to begin on final phase of 41-acre Columbus Italian Village development

30 June 2025, The Columbus Dispatch - Next Phase of Zoning Reform Will Cover 43% of City

26 June 2025, Columbus Underground - Number of Columbus-area homes for sale climbs, leading to price drop in some areas

23 June 2025, The Columbus Dispatch - Got an offer to sell your house and lease it back? Columbus experts urge caution

23 June 2025, The Columbus Dispatch - Developer enlarges plan for University District housing complex on Little Bar site

20 June 2025, The Columbus Dispatch - Downtown Columbus will soon welcome 400 new apartments and market

16 June 2025, WBNS 10TV - Ohio's youth facing affordable housing crisis

15 June 2025, Spectrum News 1 - Work Starts on First of 27 New Scattered-Site Homes

13 June 2025, Columbus Underground - Columbus apartments say residents owe thousands, threaten eviction if they don't pay

13 June 2025, The Columbus Dispatch - Ohio Housing Trust Fund Restored in State Budget Update

9 June 2025, Ohio Capital Journal/Columbus Underground - Ohio Senate added $100 million worth of housing provisions in the state’s two-year budget

5 June 2025, Ohio Capital Journal - Columbus continues affordable housing fight as some funding drops

2 June 2025, WCMH NBC4 - Columbus City Council boosts renter protection with new ordinances

2 June 2025, WBNS 10TV - Columbus Division of Housing Stability to advocate for renters, punish bad landlords

2 June 2025, The Columbus Dispatch - 75-unit affordable housing development proposed in Dublin

28 May 2025, Columbus Business First - November Bond Package to Include $500 Million for Affordable Housing

22 May 2025, Columbus Underground - Columbus approves transformation of historic YMCA into affordable housing

21 May 2025, WXYX Fox28 - Central Ohio housing prices soaring, especially near Intel plant

16 May 2025, WCMH NBC4

Beyond Ohio

- The Surprising Profits in Affordable Housing

17 June 2025, Columbia Business School- New research reveals that private landlords who invest in low‑rent properties actually earn some of the highest returns in real estate.

- Could this city be the model for how to tackle the housing crisis and climate change?

15 June 2025, NPR- Vienna uses subsidized housing to drive innovative climate design

- The Trump administration is working on a plan for time limits on rental aid

4 June 2025, NPR - The Housing Market Was Supposed to Recover This Year. What Happened?

2 June 2025, The New York Times - Why rents are rising again

2 June 2025, Axios

Appendix: Cooperatives, but not for housing

While Columbus hasn't really had housing co-ops, there have been (and still are) cooperative grocery stores. Some readers may remember the Olentangy Cooperative Grocery near Dodridge and High Street, for example. Other parts of the state also had co-op companies.

Some readers may remember Olentangy Cooperative Grocery in Old North Columbus. (Source: CML)

The New Community Cooperative Company in Dillonvale, Ohio

In eastern Ohio, a co-op founded in 1908 was visited by attendees of a conference on cooperatives held at Denison University in August of 1982 (Fedak, Dispatch, 19 July 1982). The article called Dillonvale Co-op "America's oldest existing continuously operated consumer cooperative."

Below are photos of the co-op store, inside the wholesale distribution center, and several original founding members of the 1908 c0-op pictured in a 1943 publication celebrating the organization's 35th anniversary. Cooperatives are not a new idea and they're certainly part of the American spirit of free enterprise and 'smaller is better' localism!

Photos and ephemera from The New Co-operative Company, a co-op store founded in 1908 in the town of Dillonvale, Ohio in Jefferson County. Source: Dillonvale Ohio Historical Photos, Facebook Group