💥 Achieving housing abundance and stability

Supply is just one part of our affordability crisis (which isn't all that new)

Neighbors for More Neighbors—Columbus is all about educating and mobilizing people to get engaged in community housing discourse.

We aim to add nuance, detail, and critical perspectives to a conversation that is often dominated by oversimplified assertions of ‘supply and demand.’ We’ve evolved on the issues and (usually) seek not to let the perfect be the enemy of the good. Nevertheless, our housing system deserves closer inspection if we hope to alleviate our crisis, and get ahead of it before it worsens. While we await figures from the recent point-in-time homelessness count, the Dispatch reminds us that “Last year's count by the shelter board of unhoused people found the single largest increase and an all-time high of people experiencing homelessness.”

Homelessness is one manifestation of what many people understand to be a state of crisis in American housing. But let’s take a moment to look at some foundational concepts of the pro-housing movement, as well as ask deeper questions about the so-called “crisis” of housing affordability.

What is housing abundance?

Loosely defined, housing abundance is when finding safe, adequate, and affordable housing is not difficult. When housing is not scarce. When, like many other things our economy produces (e.g. reality television shows, cute summer blouses), there is enough to go around.

What is housing stability?

Housing stability is distinct from abundance, referring to the ability to remain in one’s home without fear of displacement. This is typically sought through pro-tenant policy reforms, like preventing no-cause evictions and indexing most rent increases to inflation or cost of living metrics. Without housing stability, people are referred to as experiencing housing ‘precarity,’ a term that can also be applied to employment.

Is there an affordability crisis?

That depends on how you define “crisis.” Scholar Ricardo Tranjan suggests that the word crisis is typically something “infrequent, surprising, and widely undesirable.” Instead, the reality is that safe and adequate private rental housing has almost never been “affordable” to the lowest income-earners.

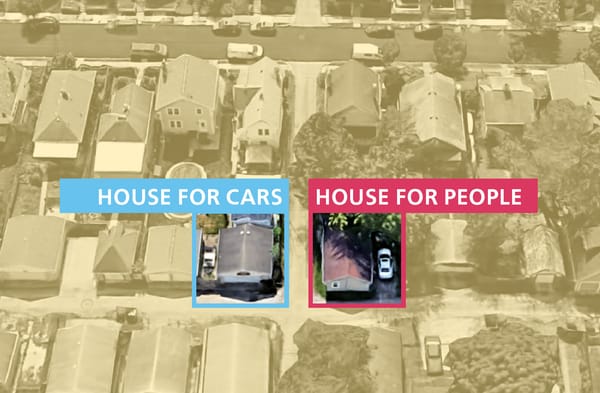

Housing, a core human need, is in a unique position as a market good for a few reasons. One is that the owners of rental housing aren’t seeking to get rid of their good in the way that, say, someone selling bananas is. Tranjan explains that since bananas spoil quickly, “it is in the interest of sellers to get rid of them, even if for a lower price than initially expected.” Housing, on the other hand, goes up in value over time. And owners often benefit financially by letting units sit vacant until someone willing to pay higher asking rents comes along.

For many actors in the business of housing, the system is working just fine. Multifamily housing developers and funders aren’t shy about asking whether too much supply will impact their bottom line—meaning renters will have too many choices and landlords will have to compete for customers by lowering rents.

On the topic of whether there’s currently a ‘housing crisis,’ it can be instructive to look to the past. A cursory search of the digital Columbus Dispatch archives returns dozens upon dozens of results for the term ‘housing crisis’ since about 1920. From federal rent control policies during the second World War to more generalized crisis states of the 1970s and 1980s, the American housing system has always had pervasive problems of affordability and access.

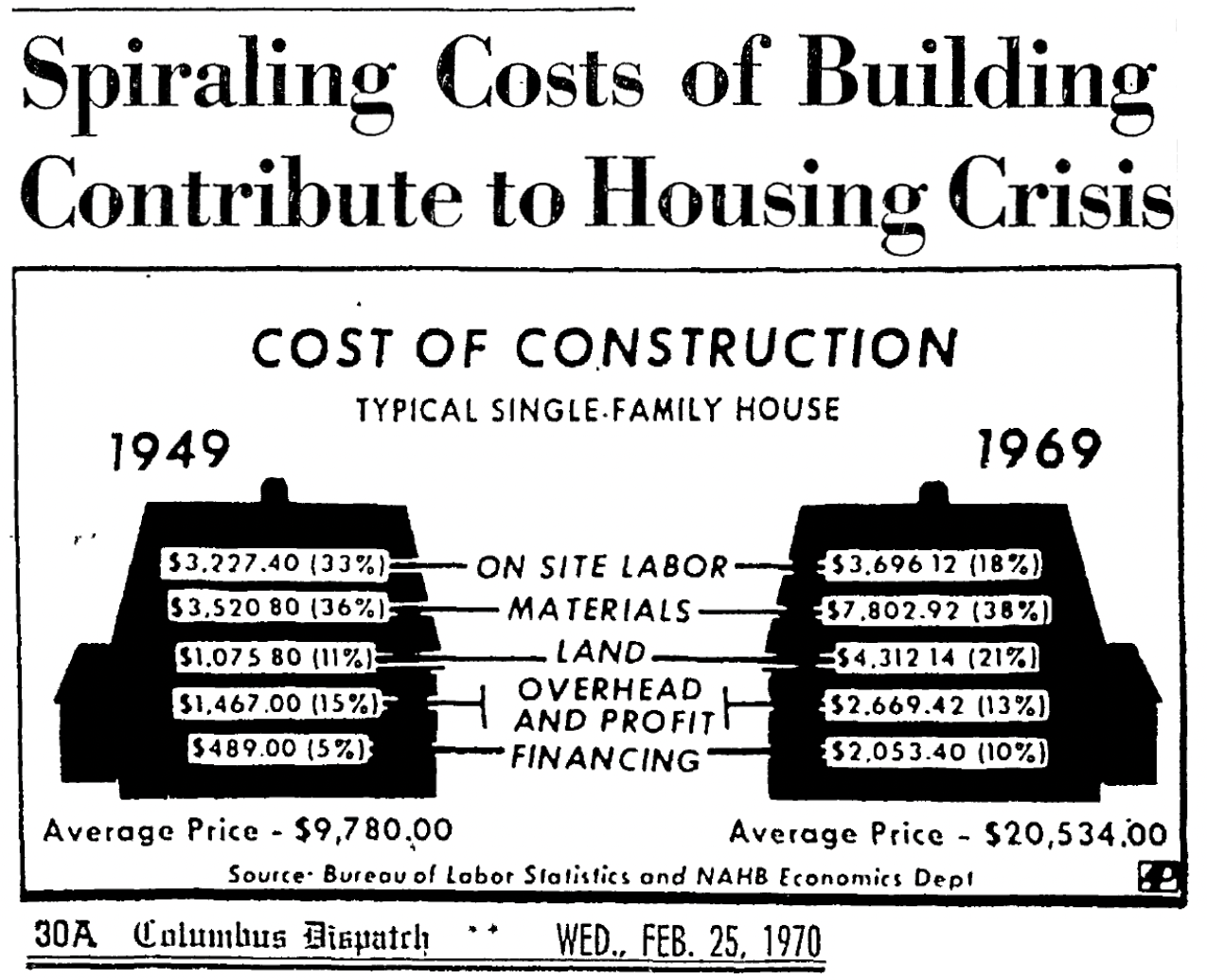

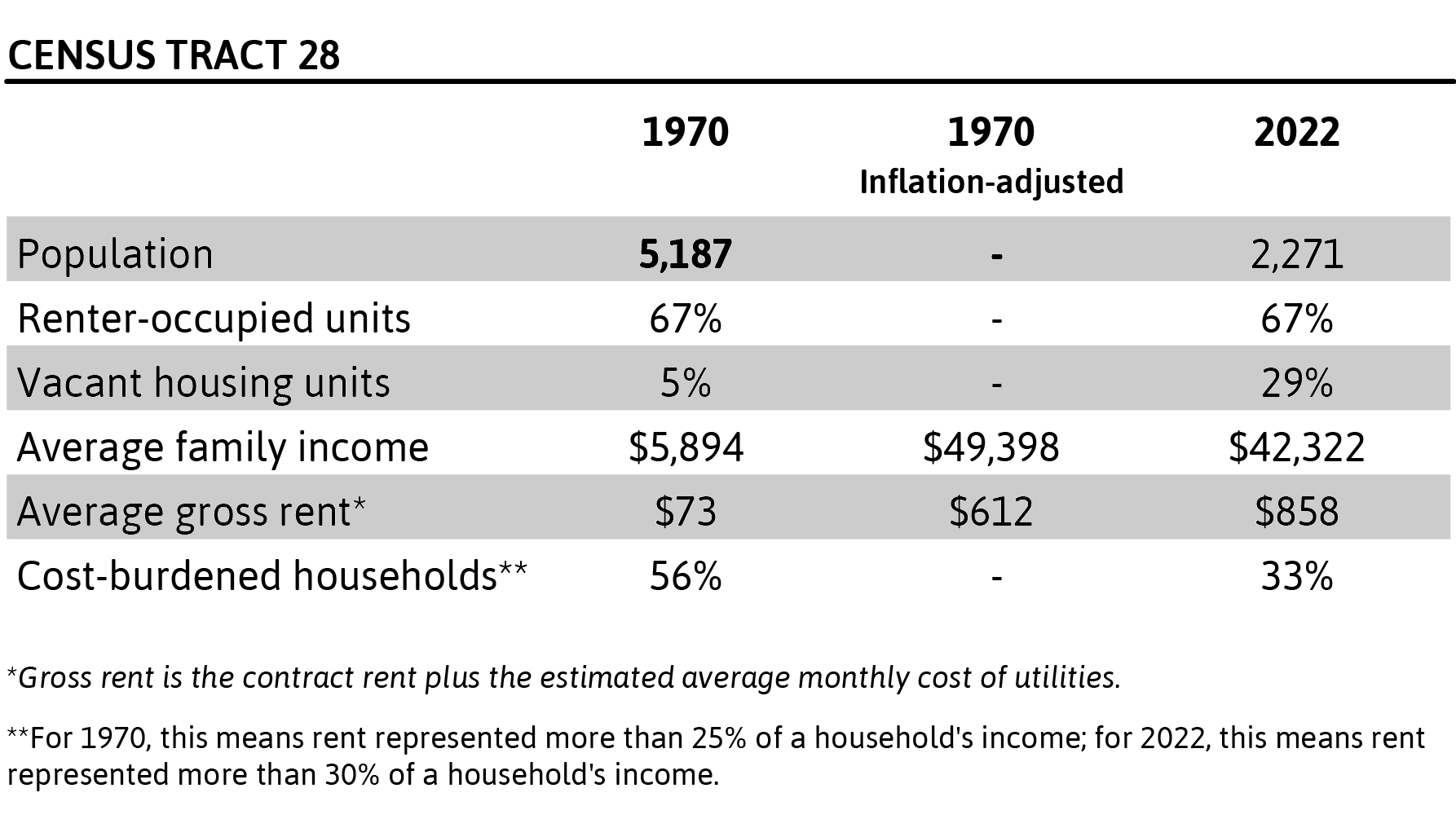

When considered in the context of persistently stagnating wages, the cost of housing has only been increasing. A quick look at one Columbus census tract on the Near East Side demonstrates how real incomes have decreased since 1970, while rents have increased. While it’s important to look at housing costs through the lens of earned income, it’s even more important to recognize the universal need for safe and decent housing regardless of an individual’s earned income.

If housing in the U.S. is currently in crisis, then we’ve been in a constant state of crisis for more than a century. That’s not to say this crisis doesn’t manifest in particularly acute ways or have localized and temporal dynamics, but it would be impossible to identify a historical period in which everyone in the U.S. was safely, stably, and affordably housed.

Policy Pitches ⚾

💸 Renter’s Tax Credit

- A renter’s tax credit allows a taxpayer who rents their main residence to receive a credit on their annual tax return based on how much they pay in rent. Like homeowners who can deduct some of what they pay toward the property, including taxes and interest on their mortgage, renters can also qualify for some renters tax credits in several states.

- For context, the federal government subsidized homeowners with $125billion between 2020 and 2024 in lost federal tax revenue to support the Mortgage Interest Deduction (Joint Committee on Taxation, 2020).

- The largest share of the MID benefits households with annual incomes of more than $100,000

⛪ “Yes in God’s Backyard”

- A proposed zoning amendment in Montgomery County, Maryland would allow the construction of multifamily housing in areas zoned exclusively for single-family residential use when associated with religious institutions

- Projects must include 30-50% below-market rent units

- Using faith-based land for multifamily housing development allows for mission alignment between pro-housing orientations of religious tenets and the need to develop housing in already built-out neighborhoods using underutilized land owned by congregations

📚 The Book Beat

Marchiel, R. K. (2020). After Redlining: The Urban Reinvestment Movement in the Era of Financial Deregulation. University of Chicago Press.

Marchiel’s portrait of a “transitioning” Chicago neighborhood during a period of white flight captures how business interests and regulations coincided to produce urban disinvestment and racial segregation.

While many private enterprises were busy profiting from accelerating urban segregation, one group of white homeowners who supported racial integration realized that institutions stopped offering financing once African Americans moved into their neighborhood. These areas were then ruthlessly targeted by panic-peddling real estate agents and word would circulate throughout the community about an area’s “transition” from white to a “riskier” composition.

This history demonstrates the power of lenders’ perceptions to determine what built forms and residential structures are worth extending credit toward.

The ways that lenders understand risk are wrapped up in cultural biases that result in unequal opportunities for borrowers based on neighborhood demographics. For example, Marchiel’s book identifies multiple cases where financial institutions (called thrifts at the time) had explicit policies to deny credit to multi-family apartment buildings and mixed-use structures—while focusing loans to single-family homes and ramping up lending in suburban areas.

One banker said any borrower seeking a loan to live in one of these neighborhoods “needs a psychiatrist” rather than a lender (p. 164).

This stigmatization set off a chain of events leading to widespread negative impacts to property values, showing how the perceptions of risk by financial professionals contributed to actively shaping reality rather than simply reacting to it. The attachment to place felt by these residents motivated them to adopt a defensive stance with a “follow the money” tactical approach, leading organizers to investigate the source of the financial regulations doing the most harm.

Reinvestment activists organized primarily around a common enemy of the “money interests,” or financial actors who stood to profit by ignoring and otherizing urban neighborhoods while simultaneously investing heavily in suburbs.

This story of neighborhood activists fighting geographic discrimination and a refusal by thrifts to extend credit to integrating neighborhoods highlights the need for government intervention to correct market forces that result in unequal outcomes and perpetuate discrimination.

🗞️ The Freshest Links of 2024 🏘

Land Value Tax Proposal in Detroit 💰

The City of Detroit is pursuing the adoption of a Land Value Tax, an alternative way to tax land that re-balances tax burden toward unproductive and vacant land.

- Could this obscure tax idea reshape American housing?: Detroit may put the land-value tax to the test

5 January 2024, Vox

Local + Regional 🌳

- Potential tiny home village could provide affordable housing for low-income Newark families

25 January 2024, The Columbus Dispatch - New affordable housing complex opens on Lockbourne Road on South Side, already leased up

22 January 2024, The Columbus Dispatch - Columbus-area home prices top record high for 2023

19 January 2024, The Columbus Dispatch - Latitude Five25 tenants to receive $1.5 million after judge signs settlement17 January 2024, The Columbus Dispatch

- Neighborhood leaders want Columbus to tighten rules regarding short-term rentals

16 January 2024, The Columbus Dispatch

National 🇺🇸

- Housing is now unaffordable for a record half of all U.S. renters, study finds

25 January 2024, NPR - A Bad Office Can (Potentially) Become a Good Apartment: The challenges and complexities of cubicles out, bedrooms in

24 January 2024, Curbed - New York Settles Suit That Said Its Housing Rules Worsened Segregation

22 January 2024, The New York Times - The Culture War Tearing American Environmentalism Apart

18 January 2024, The Atlantic - In San Francisco, Tenants Use Labor Tactics to Challenge Their Landlords

15 January 2024, The New York Times - Boston is using public buildings — like libraries — to build affordable housing. It's still pricey

8 January 2024, WBUR Boston